Arnold Van Den Berg discusses the following topics during his talk: · How he developed his investment philosophy and principles · How his experiences in the Holocaust influenced his philosophy and principles

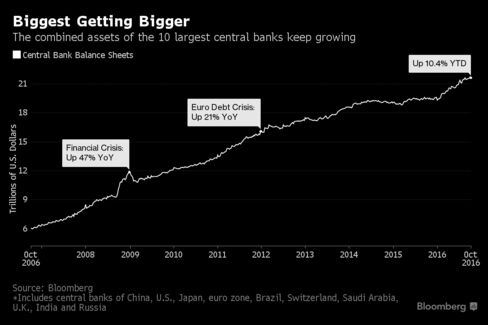

The

world’s biggest central banks are bulking up their balance sheets this

year at the fastest pace since 2011’s European debt crisis to boost

lackluster economic recoveries with asset purchases that are supporting

stock and bond prices.

The 10 largest lenders now own assets

totaling $21.4 trillion, http://www.bloomberg.com/news/articles/2016-10-16/big-central-bank-assets-jump-fastest-in-5-years-to-21-trillion

a 10 percent increase from the end of last

year, data collected by Bloomberg show. Their combined holdings grew by 3

percent or less in both 2015 and 2014.

The

accelerating expansion of central banks’ balance sheets comes as debate

rages over whether their asset purchases and continued low interest

rates are creating bubbles, especially in the bond market.

Such quantitative-easing programs are aimed at driving up the prices of

the securities they purchase to lower bond yields, encourage investment

and boost economic growth.

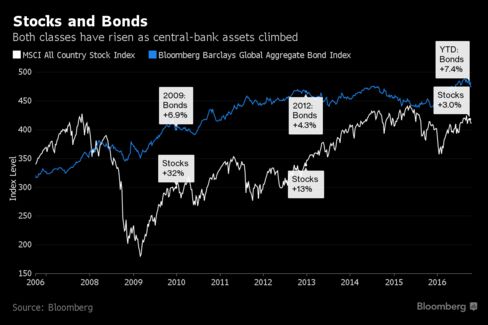

The

growth of central-bank holdings has coincided with the mostly upward

trend of stock and bond prices. As the top 10 expanded their balance

sheets by 265 percent since mid-October 2006, the MSCI All Country World

Index of equities gained 19 percent and the Bloomberg Barclays Global

Aggregate Index of bonds advanced 50 percent.

Over the past

decade, the Swiss National Bank expanded its holdings the most among

those with the largest portfolios, almost eight-fold in U.S. dollar

terms. The Bank of Russia was the least aggressive with a 68 percent

increase.

As the biggest banks’ holdings grew 10.4 percent this

year, the stock gauge gained 3 percent and the bond benchmark jumped 7.4

percent.

The

Bank of Japan and the European Central Bank together have expanded

their assets by $2.1 trillion since Dec. 31, more than accounting for

all of the top 10’s combined increase. The balance sheets of the

People’s Bank of China and the U.S. Federal Reserve fell 2 percent or

less as the Swiss and the Central Bank of Brazil boosted their holdings

15 percent or more.

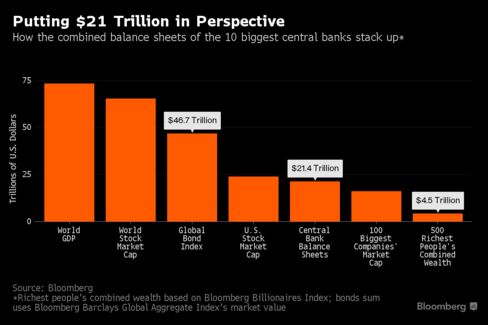

How much is $21.4 trillion?

It’s 29

percent of the size of the world economy as of the end of 2015, double

what it was in mid-September 2008, when Lehman Brothers Holdings Inc.’s

collapse sparked the global financial crisis. It’s a third of the

combined market capitalization of every stock in the world and almost

half the value of all debt in Bloomberg’s global bond index.

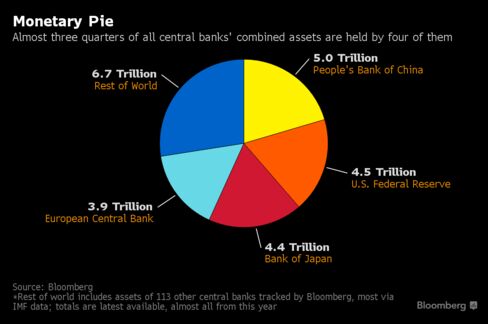

Almost

75 percent percent of the world’s central-bank assets are controlled by

policy makers in four places: China, the U.S., Japan and the euro zone.

The next six -- the central banks of Brazil, Switzerland, Saudi Arabia,

the U.K., India and Russia -- each account for an average of 2.5

percent. The remaining 107 central banks tracked by Bloomberg, mostly

with International Monetary Fund data, hold less than 13 percent.

Before it's here, it's on the Bloomberg Terminal.LEARN MORE

Investors are giving up on stock picking.

Pension

funds, endowments, 401(k) retirement plans and retail investors are

flooding into passive investment funds, which run on autopilot by

tracking an index. Stock pickers, archetypes of 20th century Wall

Street, are being pushed to the margins.

Over the three

years ended Aug. 31, investors added nearly $1.3 trillion to passive

mutual funds and their brethren—passive exchange-traded funds—while

draining more than a quarter trillion from active funds, according to Morningstar Inc.Advocates

of passive funds have long cited their superior performance over time,

lower fees and simplicity. Today, that credo has been effectively

institutionalized, with government regulators, plaintiffs' lawyers and

performance data pushing investors away from active stock picking.

In developed markets, “the pressure has gotten so great that passive has become the default,” said Philip Bullen,

a former chief investment officer at active-management powerhouse

Fidelity Investments. He and others say active management can succeed

with less widely traded assets.

The upheaval is shaking Wall Street.

Hedge-fund managers, the quintessential active investors, are facing mounting withdrawals

as they struggle to justify their fees. Hedge funds, which bet on and

against stocks and markets world-wide and generally have higher fees

than mutual funds, haven’t outperformed the U.S. stock market as a group

since 2008.

Some giants of passive investing, such as Vanguard Group and BlackRock Inc., are attracting lots of money and gaining clout in shareholder votes at public companies.

Although

66% of mutual-fund and exchange-traded-fund assets are still actively

invested, Morningstar says, those numbers are down from 84% 10 years ago

and are shrinking fast.

Performance

is driving the upheaval. Over the decade ended June 30, between 71% and

93% of active U.S. stock mutual funds, depending on the type, have

either closed or underperformed the index funds they are trying to beat,

according to Morningstar.

Moreover, because matching the performance of stock indexes is far cheaper than trying to beat them, index funds’ expenses are a fraction of what active funds charge—sometimes 1/30th or less. With interest rates near zero, fees stand out more than ever.

ENLARGE

There is a downside, according to active-investing

advocates. Passive funds are designed only to match the markets, so

investors are giving up the chance to outperform them. And if fewer

managers are drilling into financial reports to pick the best stocks and

avoid the worst—index funds buy stocks blindly—that could eventually undermine the market’s capacity to price shares efficiently.

That isn’t stopping one of the largest migrations of money in history.

“It is time to acknowledge the truth,” said a March shareholder letter from Cohen & Steers Inc., manager of real-estate and other specialized active funds. Stock

picking in its current form “is no longer a growth industry.”

Active-fund firms that don’t “position themselves for the sea change”

will be “relegated to the dustbin of history.”

This month, active manager Janus Capital Group Inc.agreed to sell itself to a British rival to diversify and help compete with lower-cost providers.

Employer-sponsored

401(k)-style retirement plans have 25% of their assets in index funds,

up from 19% in 2012, according to investment-consulting firm Callan

Associates Inc. Public pension plans had 60% of their U.S. stock

allocations in index funds in 2015, up from 38% in 2012, according to

research firm Greenwich Associates. At endowments and foundations, the

index-fund share rose to 63% from 40% in that time period.

The

biggest passive portfolio, Vanguard Total Stock Market Index Fund, now

has $469 billion in assets, nearly as much as the four largest active

funds combined. Fidelity’s 500 Index fund, at $103 billion, may soon

surpass the firm’s largest active portfolio, Contrafund, which holds

$108 billion.

Bob Chesner recently converted the $7.5

million 401(k) plan he oversees as chief operating officer of Austin,

Texas, law firm Giordani, Swanger, Ripp & Phillips LLP from a lineup

of mostly active funds to index funds.

“I was very much

a believer in active management,” he said. “I thought markets were

inefficient to the point where active management made a difference.”

A

few years ago, he noticed that the roughly 40 active funds in the law

firm’s menu were recovering from the 2008-09 market meltdown more slowly

than their benchmarks and the index funds that track them.

“That’s when it dawned on me that we were not doing something right,” he recalled.

In

the spring of 2014, over lunch, Mr. Chesner and the two other members

of the retirement plan’s executive committee decided on a change. By

going with an all-index-fund lineup, the firm’s employees would save an

average of 1.59 percentage points in annual expenses.

“When

you look at the fact that people are living longer, that makes a huge

difference” in retirement savings, said Mr. Chesner. “It’s almost a

no-brainer.”

ENLARGE

Lawsuits also are motivating investors to make changes. Over the past decade, Jerome Schlichter, a plaintiffs’ lawyer, has been suing corporations and, more recently, colleges and universities, contending the employers breached their fiduciary duty by allowing unreasonably high fees in their 401(k)-style plans.

Mr.

Schlichter’s cases, 40 in the past decade including 15 this year, “are

not saying that active management is per se imprudent,” he said.

Instead, they put the burden on a plan to show there is a reasonable

likelihood an investment will beat the market persistently after fees—“a

pretty big burden of proof,” he said, given active management’s costs

and record.

Companies and schools have generally defended their plans, calling them generous, well-designed and legal.

The

Illinois State Board of Investment, which oversees a $16 billion

defined-benefit pension plan and a $4 billion 401(k)-style plan for

state workers, voted Sept. 15 to convert the 401(k)-type plan to an all-index-fund lineup.

Board members were motivated mainly by a desire to reduce costs and make investment choices easier to understand.

With

index funds, “if you pick up a newspaper and see how the S&P

performed, you will know how your portfolio did,” said board Chairman Marc Levine. “They provide perfect transparency.”

The

fee lawsuits also influenced the decision, he said. At a recent

meeting, the board’s attorney “walked us through the potential liability

if there is harm to even a single participant,” he said. “It was quite a

wake-up call.”

Board members worried participants are

more likely to “chase performance” with active funds by piling into

portfolios that shine one year only to lag behind the next, said Mr.

Levine, a former investment banker. “If that manager concentrates the

investment portfolio and a stock blows up, that’s a potential legal

problem for us.”

The Illinois board will shift $2.8 billion from active funds at companies including Fidelity Investments, Invesco Ltd. and T. Rowe Price Group Inc. into index funds managed by Vanguard and Northern Trust Corp. The board expects the switch to reduce fees to 0.09%, from 0.37%.

Fidelity

and Invesco declined to comment. T. Rowe Price respects the Illinois

board’s decision, said a spokesman, but remains “confident in the value

added by our actively managed strategies.”

ENLARGE

When Stephen Sexauer, chief investment officer at the San

Diego County Employees Retirement Association, took over last year, the

public pension fund was paying an average of 1.1% in investment

expenses, nearly twice what comparable plans in other California

counties paid, without earning better returns, he said.

“You

have to ask yourself, ‘If we’re spending all this money on fees,

where’s the evidence of success?’ And it’s really hard to find,” he

said.

So the plan moved 25% of its assets—$2.5 billion at the time—into index funds charging average fees of .05%.

Mr.

Sexauer also placed $100 million in a so-called balanced portfolio of

70% stock index funds and 30% bond index funds. All the plan’s other

investments will be pitted, in a kind of tournament, against that

portfolio. If they don’t deliver, they will be axed, he said.

The

internal index fund “is kind of like Pac-Man,” he said. “If it

outperforms over time, eventually a capable administrative assistant

might be able to run the entire investment department, and we’d be OK

with that.”

“What’s going on is a generational shift,” said John D. Skjervem,

54 years old, chief investment officer of the Oregon State Treasury,

which oversees $90 billion in public assets and trust funds. “Guys like

me are moving in, and we had education that was empirically more

rigorous than the prior generation’s.”

Mr. Skjervem has

an M.B.A. from the University of Chicago Booth School of Business, known

for teaching that markets are efficient and stock picking is largely a

waste of time.

“When you adopt an empirical framework,

you expose a lot of storytellers,” he said. “I’m very uncomfortable in

the realm of the narrative. I want to listen to the data instead.”

Since John D. Skjervem

became chief investment officer of the Oregon State Treasury in 2012,

Oregon has shifted about $4 billion out of active funds, or about 15% of

the pension plan’s public-equity assets.

Photo:

Bruce Ely for the Wall Street Journal

Since Mr. Skjervem joined in 2012, Oregon has shifted about

$4 billion out of active funds, or about 15% of the pension plan’s

public-equity assets. Eventually, he said, the state may use traditional

active management for as little as 20% of its total public stock and

bond assets.

Over the past three years, Fidelity,

historically renowned for its active management, has launched nearly

two-dozen index mutual funds and ETFs, bringing its total passive lineup

to approximately 50 funds. Currently 12% of the $2.2 trillion it

manages is in index strategies, twice the level five years ago.

Fidelity

executives are “trying to help educate the marketplace that there is a

difference between all active and good active,” said Tim Cohen, the firm’s head of global equity research. In research released in March,

the firm found that among the 25% of all active U.S. large-stock mutual

funds with the lowest fees between 1992 and 2015, those from the five

largest firms outperformed their benchmarks, on average.

That

message hasn’t been an easy sell. “It’s been a tough period for the

industry, and flows certainly reflect that,” Mr. Cohen said.

Federal

regulations are pressuring investment fees, accelerating the move to

indexing, which is an easy way to cut costs. In 2012, the Labor

Department started requiring greater fee disclosure in 401(k) plans. The

fees on retail mutual funds in large 401(k)s have since fallen by 12%,

according to Callan Associates.

In April, the Department of Labor’s new so-called fiduciary rule is

scheduled to go into effect. Financial advisers overseeing individual

retirement accounts will have to demonstrate that their decisions are in

the best interests of their clients, a change that is expected to lead

to more fee-based accounts rather than accounts that use commissions

with the potential to lure brokers. By using index funds in accounts

already bearing an annual fee, brokers can help keep overall costs down.

BlackRock this month said it would lower costs on more than a dozen ETFs in light of the new rule. Morningstar expects the regulation could push as much as $1 trillion into passive investments.

Mr.

Bullen, the former Fidelity executive, now manages money for wealthy

families and uses a mix of passive and active funds. He also serves on

the investment committee of the approximately $480 million endowment of

the Whitehead Institute for Biomedical Research at the Massachusetts

Institute of Technology.

Though several of the eight

committee members are current or former heads of active firms, the

committee reached a unanimous decision to cease using active funds for

publicly traded securities, according to Mr. Bullen and others.

“The case for passive is being made so well and so clearly,” said Mr. Bullen, “it has become common wisdom.” Write to Anne Tergesen at anne.tergesen@wsj.com and Jason Zweig at intelligentinvestor@wsj.com

Desperate for yield, investors are buying government

bonds that come due further and further in the future. If you lend your

money to the government, you expect to get it back. It’s not for nothing

that British government bonds are ‘gilt-edged,’ and the U.S. Treasury

yield is considered ‘risk-free’ in financial models. What could possibly

go wrong?

Unfortunately, a lot. A small move in the yield on

these increasingly popular 40-, 50- and sometimes even 100-year bonds

can have a crippling effect on their capital value.

Anyone who might sell before they mature (hint:

that’s everyone alive today for the longest-dated bonds), should

consider how they'd feel if their supposedly safe bond had lost a

quarter of its value in two months. It happened to the rock-solid German

30-year bund, just last year.

This calculator lets you play with interest rates and

see just how big an impact changes to yield can have on the price of

long-dated bonds. You might be surprised by how big the losses could be,

if the drops in yield of the past couple of years go into reverse.

See how changing the yield moves the price of government bonds:

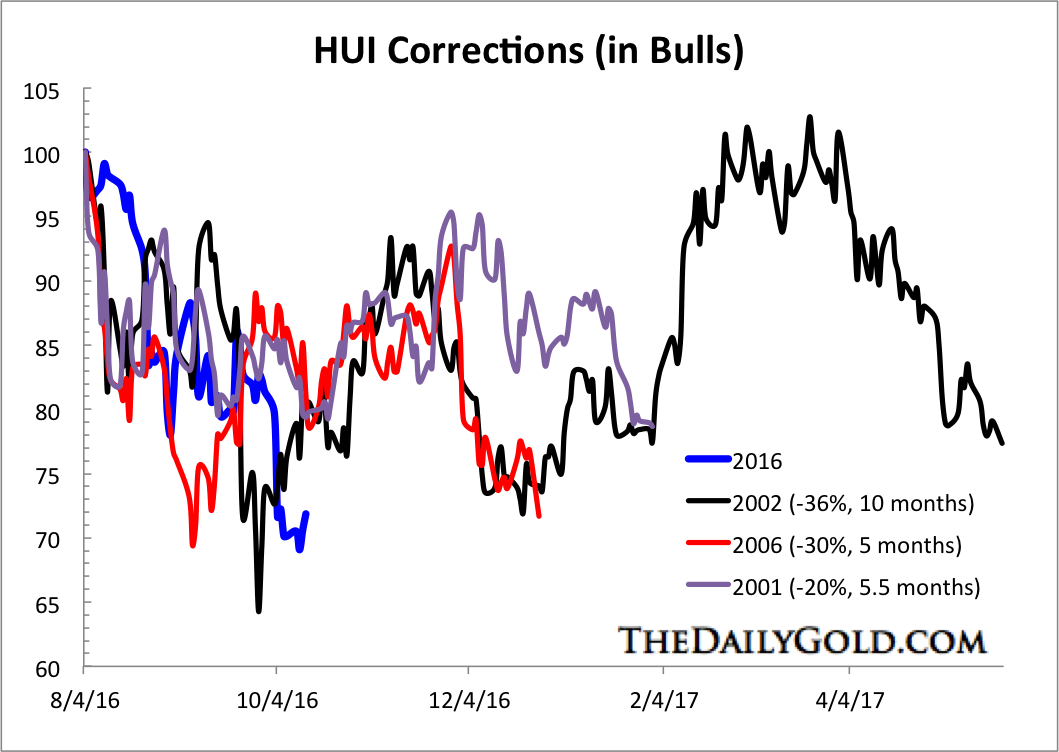

The

gold stocks are clearly in correction mode. The large caps (HUI, GDX)

have corrected 30% while the juniors (GDXJ) have held up well in

comparison by correcting the same amount. Given a number of factors (the

size of the previous advance, the recent technical damage, stronger US$

index and rising yields) the gold stocks should continue to correct and

consolidate in a larger sense. To gauge a potential path forward we

present a new analog chart and compare the current correction to those

from past markets. The

chart below plots the current correction in the HUI index in comparison

to the corrections in 2001, 2002 and 2006. Each correction followed

very strong advances. The 2001 and 2002 periods are the best comparison

to today. The recent rebound originated from a potential secular low

(like 2001) and lasted six to seven months (like 2001). However, the

rebound was much stronger than in 2001 and reached an extreme overbought

point (like 2002). The HUI has already corrected 31%, which is much

closer to the 2002 correction. Only time will tell how long the

correction lasts but my view is it is more likely to last around six

months than the 10 months seen in 2002.

Gold Stocks Correction Analog

The

other important point to mention is every correction formed a typical

A-B-C or down-up-down pattern. In other words, each correction served

investors two buying opportunities (and three in the case of 2002).

While we are likely at a short-term buying opportunity now, probability

tells us that another one is coming in the next several months. A

variety of technical indicators (various moving averages, pivot points,

Fibonacci retracements) gave us downside targets of GDX $22 and GDXJ

$34-$35. That degree of downside is inline with the correction analog

chart. While it may take another week for the sector to find a

short-term low, the outlook over the next several weeks appears

positive. Continue to accumulate on weakness and don’t be afraid to

exercise some patience as more buying opportunities will be ahead. For

professional guidance in riding the uptrend in Gold, consider learning

more about our premium service including our favorite junior miners

which we expect to outperform into 2017.

Mirror, mirror on the wall, which asset is most mispriced of all?

According to a Goldman Sachs alum who predicted the financial crisis in

2008, it’s gold.

The precious metal should be a lot more

expensive when the likelihood of a global financial collapse and a move

toward negative interest rates is accounted for, says Global Macro Investor founder Raoul Pal, who now sees a U.S. recession within 12 months.

Recent losses for gold may have dented investor confidence. Gold

GCZ6, -0.38%

is up 18% this year, but the

first full week of October marked its worst seven-day performance in

over three years; it also posted a three-month loss of nearly 6% on a

continuous basis.

Uncertainty about Brexit and the timing of a

Federal Reserve rate hike triggered a rush into the dollar, which often

moves inversely to the metal. (Higher rates can work against gold, but

the metal becomes a safe haven if the economy slows.)

“As

we get to negative interest rates, gold is a good place to park your

cash,” said Pal, who discussed his outlook with MarketWatch in a

September interview and a follow-up conversation over email.

“I’m

not a gold bug,” the former GLG Global Macro Fund co-manager — who is

also watching the dollar closely — “but this is the currency I would

choose now.”

Pal, an economist and strategist, also co-founded Real Vision TV, which conducts interviews with prominent investors. Many of his recent guests share his enthusiasm for gold, according to Pal.

“All the really serious thinkers are interested in gold,” he said.

How a U.S. recession could boost gold and the dollar

Pal’s

core presumption — one he’s held since 2014 — is bad news for the U. S:

He is convinced the country is headed for recession within a year. “The

business cycle points to that,” he said, “and 100% of all two-term

elections have had a recession within 12 months since 1910.”

His view contrasts with the Federal Reserve’s own indicator, based on corporate-bond spreads, that predicts just a 12% chance of a pullback in the next year.

But Pal does have some prominent company: Savita Subramanian, Bank of America’s head of equity strategy, recently predicted the same; Janus Capital’s Bill Gross spoke of a lagging U.S. recovery in his September investment note; and bond investor Jeffrey Gundlach showed a chart during a recent webcast that revealed the start of a recession. And Wilbur Ross sees one coming in 18 months.

Should

his prediction come true, Pal says, gold prices could double. If

central banks want to get active and combat a slowing economy, he says,

they will try to stimulate the economy via printing money or more

easing, all of which plays “into the hands of gold.”

This view

brings Pal to the asset he favors most over the next year out of bonds,

equities, currencies and commodities: the dollar. He told MarketWatch

he’d buy U.S. dollars, selling the euro, pound and Aussie dollar; he

expects the euro

EURUSD, -0.7506%

to eventually drop to 75 cents

against the dollar — about 3% below current levels — over time.

“The

world has shifted because of negative interest rates,” Pal said. “We

know the dollar will go higher, [and] gold may outperform over time, the

reason being because of negative interest rates. If I get it right, I

have dollars and gold…I don’t make much of a loss if that correlation

breaks.”

Year-to-date, the dollar index

DXY, +0.50%

is down nearly 1%, which some

blame in part on an inactive Fed. Interest-rate increases can have a

positive effect on a country’s currency by making it more attractive to

foreign investors.

But Pal insists that his dollar call is not

tethered to central bank policy, saying investors should let go of the

belief that those institutions are like “the Wizard of Oz.” Investors,

Pal said, believe the Fed’s policy choices can keep stocks from falling

even as Japan and Switzerland have proven otherwise. Read: Central banks ‘have never been on thinner ice’

The

Bank of Japan “has done more easing, as has the Swiss,” Pal said. “It’s

not achieved anything. Stock markets there have fallen, yet the market

wants to believe the Fed that there is an implicit put on the stock

market in the U.S.”

Switzerland has had negative interest rates in place since early 2015, yet stocks

SMI, +1.12%

fell 1.6% in 2015 and are down nearly 10% so far this year.

Japan moved to negative interest rates this year, yet the Nikkei 225

NIK, +0.49%

is down nearly 12%.

Real Vision

3-month Libor (inverted) versus Deutsche Bank shares

He believes the market is

currently short the dollar and should a banking crisis crop up in

Europe, he says, euros will get less attractive as investors prefer

dollars. In a recent interview on Real Vision, Pal discussed the problems at Deutsche Bank

DB, +0.71%

— but also how the problems extend far beyond Germany’s borders.

Spanish banks — ones like Banco Sabadell

SAB, +0.81%

Banco Popular

POP, +0.59%

— they’re all in free fall,

[at] all-time lows,” Pal said. Italian banks, with still unresolved bad

debt issues, are still a problem, and then Swiss and U.K. banks also

look unwell, he said.

“I think it’s the start of something,” he said of Deutsche Bank’s woes. Read: How Deutsche Bank is Lehman Brothers and how it isn’t

The

dollar, Pal said, also looks favorable against the backdrop of the

three-month U.S. dollar Libor (London interbank offered rate), the

benchmark rate some of the world’s biggest banks charge each other for

short term loans. When those rates are rising, he says, dollars are more

attractive.

In the last 12 months, Libor has nearly tripled, he said, moving from 0.31% to 0.88%.

“It

is also a sign that there is distress among dollar borrowers abroad, so

they might need to buy dollars to close out their risk,” said Pal.

Financial institutions, in other words, are fretting about potential

market downside, and when they get worried, the Libor moves higher.

The one chart he uses to track economic cycles

Pal is not a fan of U.S. stocks — the S&P 500 index

SPX, +0.22%

is up just 3.7% so far in 2016 —

largely because of what he sees in a chart he says that has failed him

just once when he didn’t trust it. Now, he says, it’s telling him his

recession prediction is spot on.

That chart is the Institute for Supply Management index,

which is based on surveys of more than 300 manufacturing firms and

gauges the health of the industry. The ISM rebounded in September, to

51.5% from 49.4% the previous month. But economists still say the U.S.

manufacturing sector faces challenging conditions.

“There’s a

difference between the narrative, which is what you’re being told,

versus the reality of the economic data,” said Pal. “It’s in no one’s

interest ahead of the election to say the U.S. economy is a mess —

[that] world trade freight shipments, container shipments, retail sales,

restaurant sales, factory orders, durable orders are all showing a

recession.”

Pal says the ISM correlates well with U.S. assets.

“It peaked in 2011 and has been bouncing around 50 for a while now,” he

said. “The moment it starts to get to 47, 46, the odds of a full-on

recession explode to 85%. We’re very close now, getting to the point

where the probability is very high.”

Real Vision

Pal’s go-to chart showing ISM versus the S&P 500 (year over year)

The ISM is one reason he’s

not keen on U.S. stocks, as he says he prefers to be underweight when

they are near all-time highs, then wait for the business cycle to bottom

— generally, 12 to 18 months after the start of a recession based on

past bear markets — before getting back in.

“It could be a

shallower recession,” Pal says, but “the probability is that most last

around that period of time and investors need to be aware of that.” (A

fuller explanation of his thinking can be found in a June video Real

Vision posted on YouTube.)

And Pal urges investors not to

expect Fed interest rate increases to sustain a bull market. Even if the

central bank raises rates several times over the next two years, he

says, they will still be low. “Interest rates follow the economic cycle

and do not lead it. As the economy weakens, the government cuts interest

rates.”

In other words, he says the Fed is always reactive — never proactive.

More from MarketWatch

Central banks have leapt to the forefront of public

policy-making. They have taken responsibility for lowering interest

rates (and keeping them low), for maintaining stability of financial

institutions and markets and for buying up large-scale quantities of

government debt to help economies recover from recession. Now it seems

that they have become important, too, in building up holdings of

equities to increase depleted yields on their much-increased reserves of

foreign currencies.

Central banks may be over-stretching

themselves. Jens Weidmann, president of Germany's Bundesbank – which

retains a highly important role in the euro area – spoke yearningly

last week of the need for "central banks to shed their role as

decision-makers of last resort and, thus, to return to their normal

business". He said this "would help to preserve the independence of

central banks, which is a key precondition to maintaining price

stability in the long run."

Central banks' foreign

exchange reserves have grown unprecedentedly fast – especially in the

developing world. The same authorities that are responsible for

maintaining financial stability are often the owners of the large funds

that add to liquidity in many markets and can cause the risk of

overheated asset prices.

Evidence of equity-buying by

central banks and other public sector investors has emerged from a

large-scale survey compiled by Official Monetary and Financial

Institutions Forum (OMFIF), a global research and advisory group. The

OMFIF research publication Global Public Investor (GPI) 2014, launched

on June 17 is the first comprehensive survey of $29.1 trillion worth of

investments held by 400 public sector institutions in 162 countries.

The report focuses on investments by 157 central banks, 156 public

pension funds and 87 sovereign funds, underlines growing similarities

among different categories of public entities owning assets equivalent

to 40% of world output.

The assets of these 400 Global

Public Investors comprise $13.2 trillion (including gold) at central

banks, $9.4 trillion at public pension funds and $6.5 trillion at

sovereign wealth funds. In the aftermath of the financial crisis,

different forms of "state capitalism" have come to the fore, the report

says: "Whether or not this trend is a good thing may be open to

question. What is incontestable is that it has happened."

Sovereign

wealth funds and public pension funds are well known to have become

large holders of company shares on international stock markets. The

best-known example is the Norwegian sovereign fund, Norges Bank Investment Management

(NBIM), with $880bn under management of which more than 60% is invested

in equities. The fund owns on average 1.3% of every listed company

globally.

It now appears that NBIM has rivals from a number of unexpected sources. One is China's State Administration of Foreign Exchange (SAFE), part of the People's Bank of China, the biggest overall public sector investor, with $3.9 trillion under management, well ahead of the Bank of Japan and Japan's Government Pension Investment Fund (GPIF), each with $1.3 trillion.

SAFE's

investments include significant holdings in Europe. The PBoC itself has

been directly buying minority equity stakes in important European

companies.

Another large public sector equity owner is Swiss National Bank,

with $480 billion under management. The Swiss central bank had 15% of

its foreign exchange assets – or $72 billion – in equities at the end of

2013.

Central banks have been trying to compensate for

lost revenue caused by sharp falls in interest rates driven by official

institutions' own efforts to repair the financial crisis. According to

OMFIF calculations, central banks around the world have foregone $200

billion to $250 billion in interest income as a result of the fall in

bond yields in recent years. GPIs as a whole appear to have built up

their investments in publicly quoted equities by at least $1 trillion in

recent years, in a trend that is now probably irreversible.

These

shifts have important implications for transparency and accountability

of official asset management. Sovereign funds have adopted the

so-called Santiago Principles on transparency, but central banks have

not signed up to any comparable code.

Edwin "Ted" Truman, a former senior Federal Reserve official, now a senior fellow of the Peterson Institute for International Economics, writes in GPI 2014:

"One of any government's major responsibilities is managing the

country's international assets. Reforms are urgently needed to enhance

the domestic and international transparency and accountability for this

activity – in the interests of a better-functioning world economy." David Marsh is managing director and founder of the Official Monetary and Financial Institutions Forum in London.http://www.usatoday.com/story/money/markets/2014/06/15/david-marsh-new-force-in-world-markets-global-public-investors/10548183/

Jeremy Siegel's latest column in Yahoo Finance responds to John Hussman and others, who argue that Siegel's irrational bullishness is setting him up to be

come a modern-day Irving Fisher. Siegel's response: The critics are

wrong, profit margins are fine, valuations should be higher, and stocks

are going up.

Siegel's main arguments are these:

The hand-wringing about "record-high profit margins soon

reverting to means" is misplaced because 1) a greater percentage of U.S.

corporate profits are coming from international operations, which

aren't affected by U.S. GDP, and 2) a greater percentage of overall U.S.

profits are now captured by public U.S. companies instead of private

ones.

Innovations in the financial system, namely lower trading costs

and smarter central banks, have reduced the equity risk premium. Thus,

stocks should now trade at an average P/E of about 20-times, instead of

the long-term average of about 14-times.

Siegel, in other words, believes that "it's different this time." And that's reasonable--because sometimes it is

different this time (the most salient example being a permanent change

in the relationship between bond yields and dividend yields after the

U.S. went off the gold standard--a change that cost many "prudent"

investors to miss decades of gains). Of course, more often than not,

it's NOT different this time, and those who argue that it is end up with

egg on their faces (believe me--I know).

I'll wait for Hussman, Grantham, Smithers, DeLong and others to

respond to Siegel's arguments before taking a strong stand here. I will

simply suggest that the big lesson from most major bull markets is

this: anytime someone argues that "it's different this time," the burden

of proof ought to be on them (as opposed to on bears who

appear to be "wrong" because the market keeps going up). With this in

mind, I'd like to see more data from Siegal backing up his profits

argument--a chart showing the percentage of U.S. profits generated from

international operations over time, for example, as well as a chart of

global profits relative to global GDP (are profit margins at record

highs globally, as well?).

The "risk premium" argument obviously won't be settled until after

the fact, but in my mind there's an easy counter to that one: Today's

risk premium is low because stocks haven't been that risky

recently--even with the crash of 2001-2002, global equities are sharply

higher than they were 10 years ago. Go through a couple of decades of

stagnation, meanwhile, like the periods that followed market highs in

1929 and 1966, and investors won't give a damn about low transaction

costs or more enlightened central banks. Instead, because stocks will

seem like the worst investment idea anyone ever thought of, investors

will once again demand a huge equity risk premium.

ENLARGE

ENLARGE

ENLARGE

ENLARGE

ENLARGE

ENLARGE

Real Vision

Real Vision

Real Vision

Real Vision

Jeremy Siegel's latest column in Yahoo Finance responds to John Hussman and others, who argue that Siegel's irrational bullishness is setting him up to be

come a modern-day Irving Fisher. Siegel's response: The critics are

wrong, profit margins are fine, valuations should be higher, and stocks

are going up.

Jeremy Siegel's latest column in Yahoo Finance responds to John Hussman and others, who argue that Siegel's irrational bullishness is setting him up to be

come a modern-day Irving Fisher. Siegel's response: The critics are

wrong, profit margins are fine, valuations should be higher, and stocks

are going up. Jeremy Siegel's latest column in Yahoo Finance responds to John Hussman and others, who argue that Siegel's irrational bullishness is setting him up to be

come a modern-day Irving Fisher. Siegel's response: The critics are

wrong, profit margins are fine, valuations should be higher, and stocks

are going up.

Jeremy Siegel's latest column in Yahoo Finance responds to John Hussman and others, who argue that Siegel's irrational bullishness is setting him up to be

come a modern-day Irving Fisher. Siegel's response: The critics are

wrong, profit margins are fine, valuations should be higher, and stocks

are going up.